What is a Subsidized Student Loan? – Simple Rules

Introduction

A subsidized student loan is an important financial tool for college students who need to borrow money for their tuition and fees. These loans help cover the cost of education for those who may not be able to afford it without assistance. But what makes a subsidized student loan different than an unsubsidized one? And what are the pros and cons of taking one out? In this blog post, we’ll answer these questions and more. Keep reading to learn everything you need to know about subsidized student loans and how they work.

What is a Subsidized Student Loan?

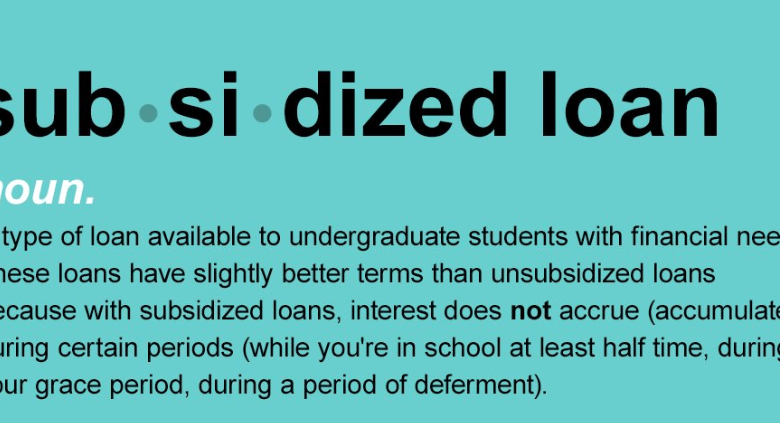

A subsidized student loan is a type of financial aid that is provided to students by the government. The interest on the loan is paid for by the government, making it easier for the student to repay the loan. Subsidized student loans are available to undergraduate and graduate students who demonstrate financial need.

How Does a Subsidized Student Loan Work?

Assuming the reader has a general understanding of how student loans work, we’ll dive right into how a subsidized loan works.

A subsidized loan is one where the government pays the interest while the student is in school. This can save the borrower a lot of money, as it means they don’t have to start paying off the loan’s interest until after graduation.

The subsidized loan program is need-based, meaning that only students with financial need are eligible for this type of loan. The government will determine your need based on information you provide in your Free Application for Federal Student Aid (FAFSA).

If you’re eligible for a subsidized loan, you’ll be offered one as part of your financial aid package. You can then choose to accept or decline the loan. If you accept it, you’ll be responsible for repaying the entire loan, including both principal and interest, after you graduate or leave school.

It’s important to note that subsidized loans are only available for undergraduate students. If you’re pursuing a graduate degree, you’ll have to take out an unsubsidized loan, which accrues interest from the day it’s disbursed.

Pros and Cons of a Subsidized Student Loan

There are both pros and cons to taking out a subsidized student loan. On the plus side, these loans offer borrowers a lower interest rate than unsubsidized loans. Additionally, the government pays the interest on subsidized loans while the borrower is in school, during their grace period, and during any deferment periods. This can save borrowers a significant amount of money over the life of their loan.

On the downside, subsidized loans are only available to students with financial need as determined by the FAFSA. Additionally, these loans have a shorter repayment period than unsubsidized loans, meaning that borrowers will have to start making payments sooner. Finally, subsidized loans are subject to annual and aggregate lending limits, which could impact how much money a student is able to borrow.

Who is Eligible for a Subsidized Student Loan?

A subsidized student loan is a need-based loan available to undergraduate students who demonstrate financial need as determined by the Free Application for Federal Student Aid (FAFSA). Students with the highest levels of financial need are awarded the loans.

The U.S. Department of Education pays the interest on subsidized loans while the borrower is in school at least half-time, during the grace period, and during deferment periods. repayment begins six months after the borrower graduates or drops below half-time enrollment.

How to Apply for a Subsidized Student Loan

Assuming you’re referring to a subsidized federal student loan, the process is as follows:

1. You must complete the Free Application for Federal Student Aid (FAFSA®) form to apply for a Direct Subsidized Loan or any other type of financial aid from the U.S. Department of Education. You’ll need your and your parents’ most recent federal income tax returns, W-2s and other records of money earned. Be sure to list all schools you’re interested in attending on your FAFSA form so that your information can be sent to them.

2. After your FAFSA form has been processed, you’ll receive a Student Aid Report (SAR). The SAR summarizes the information you provided on your FAFSA form and will tell you if you’re eligible for a Direct Subsidized Loan. If you are eligible, the SAR will also provide your Expected Family Contribution (EFC). This is the amount that is used to determine how much financial aid you’re eligible to receive from all sources—federal, state and institutional.

3. Once you’ve determined which school you’ll be attending, contact the financial aid office at that school and ask about the application process for federal student loans. The financial aid office will also inform you of any additional documentation they may require such as proof of citizenship or an acceptable Selective Service registration status if you’re a male between 18-25 years old.

Alternatives to a Subsidized Student Loan

There are a few alternatives to a subsidized student loan. One option is to take out an unsubsidized student loan. This type of loan does not have the same interest rate subsidy as a subsidized loan. So the borrower is responsible for all interest that accrues on the loan. Another alternative is to find a private lender who is willing to give you a loan for your education. Private loans typically have higher interest rates than federal loans. But they can be more flexible in terms of repayment options. You can also look into scholarships and grants as ways to help finance your education without taking on debt.

Conclusion

In conclusion, a subsidized student loan is an excellent way to help reduce the cost of college expenses. By understanding how these types of loans work, you can make sure that you take advantage of all the benefits. They offer and ensure that your financial future remains secure. With this knowledge in hand, you can go ahead . Aand start looking for a loan that fits your needs and apply for one today!